Have you put your money into a real estate property, and thinking it’s time to gain the benefits of your investment? There are 2 ways to go: selling your unit or renting it out. But you need to consider several elements when it comes to capital growth vs. rental income.

Before selling your property or renting it out, there are various factors you need to take into account, and on top of those come your financial goals.

This article will tell you all you need to know about capital growth vs. rental income, from their pros & cons, to what questions you need to ask yourself before picking the right strategy for you.

Capital Growth vs. Rental Income

Understanding the difference between capital growth and rental yield would help you decide which path to take to get the best return on investment (ROI).

Capital growth is the increase in the property’s market value over time. It refers to the difference between the purchasing cost and the current selling price. Several factors influence its evaluation, such as:

- Market demand and trend

- Location

- Infrastracture

- Inflation

Let’s take a look at an example of how to calculate your property’s capital growth rate.

If you bought the unit for 400,000 EGP, and after one year it costs 500,000 EGP, then:

- Current price – purchase price: 500,000 – 400,000 = 100,000 (Increase)

- Increase/purchase price: 100,000 / 400,000 = 0.25

- 0.25 x 100 = capital growth of 25%

Regarding rental yield, it is how much you should expect annually when you decide to rent out your property vs. the unit’s purchase price. Various elements affect rental income, such as:

- Rental demand

- Rent rates in the area

- Maintenance costs

The gross rental yield would provide you with a general overview. Next is an example of how to calculate it.

If you bought your property for 400,000 EGP, and its annual rental would be 50,000 EGP, then:

- Annual rental income/purchase price: 50,000 / 400,000 = 0.125

- 0.125 x 100 = gross yield of 12.5%

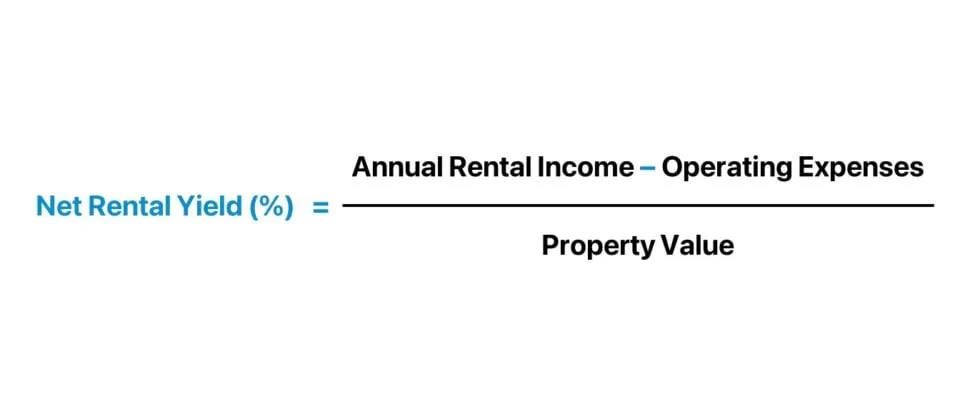

On the other hand, the net rental yield gives you a clearer, more accurate image, taking into consideration other costs, such as property maintenance. With the same example mentioned above, you subtract the additional costs of 5,000 EGP. Then:

- Annual rental income – costs / purchase price: 50,000 – 5,000 / 400,000 = 0.1125

- 0.1125 x 100 = net yield of 11.25%

Your financial goals decide which is better for you: selling and gaining one-time capital growth vs. property rental for an ongoing income. So the first question to ask yourself is whether you want the cash now or are looking for passive income over time.

There are other key factors to consider as well when deciding which strategy is the best for you.

Capital Growth vs. Rental Income: Factors to Consider

Both strategies have pros and cons, but the thing is, neither of them is suitable for all investors all the time. The factors you need to consider before deciding whether to sell your property or rent it out include:

- Market Condition and Demand: Getting to know if your property’s location is gaining appreciation and the rents in the area.

- Risk Tolerance: Property management is stressful, and the process itself is filled with ups and downs, and it all depends on the market’s condition. That’s why studying the current state would help you decide.

- Tax Implications: This factor varies according to the property type and by country. In Egypt, you have to pay taxes on rental income, unless the property’s annual rent is less than 24K EGP. There are also taxes on selling and transferring the property’s ownership.

Both strategies have pros and cons. So, how to decide: capital growth vs. rental income?

For the best return on investment, you need to examine what you will gain and the disadvantages to expect.

Learn about ROI (+How to Calculate It)

Selling vs. Renting Your Property: Pros & Cons

Understanding the pros and cons of capital growth vs. those of rental income would help you pick the best plan of action.

Starting with selling your property for capital growth, its pros include:

- If timed well, there is a higher potential for a better ROI.

- There is no ongoing property management or expenses after selling.

- Gaining a large cash upfront would help you reinvest it in another opportunity and diversify your portfolio.

- Reduces potential risks and downturns.

Regarding the cons, they include:

- The probability of capital gain taxes.

- You may miss potential future growth in your property’s value.

Pros & Cons of Renting Your Property

On the other hand, when it comes to the pros of renting out your property, they are:

- Regular cash flow and monthly rental income.

- Long-term potential for capital growth.

- A hedge against inflation, as rents increase according to the inflation rate.

- May help you cover mortgage payments and other expenses.

The cons of renting your unit include:

- Dealing with property management and issues.

- Ongoing costs, whether in the case of property damage or property management in general.

- Rental income is taxable.

- Less flexibility if you decide to sell it.

In a nutshell, selling for capital growth vs. renting out for rental income:

|

Factor |

Selling |

Renting |

|

Profit Time Interval |

Immediate | Long-term passive income |

| Cash Flow | One-time capital gain | Ongoing income |

| Timing | Requires selling at the right time (the highest market demand) | Less influenced by short-term market fluctuations |

| Property Management & Maintenance | None after selling | On-going process |

| Appreciation Potential | Losing possible future gains after selling |

Potential long-term growth |

Both strategies carry unmatched benefits, so are you wondering if you can combine them? The answer is Yes. In case it isn’t the best timing for selling your property, you can merge both for a higher ROI.

You can simply rent it for a while till the real estate market thrives, and then sell it at a higher price.

Egypt’s real estate market is flourishing, and it is one of the best countries to invest in. This makes the capital growth vs. rental income dilemma only a matter of time.

In case you decide to rent out your property, there are several ways to maximize your income.

Maximize Your Rental Income

To increase your rental income, you have to boost your property value. You can achieve this by:

- Renovations and enhancing your property’s appeal.

- Adding value features, such as high-speed WiFi, may be small, but would give grounds for higher rent.

- Furnishing your property.

- Avoid major repairs by staying on top of maintenance and property management.

- Increase rental strategically by reviewing and studying the market well.

Furthermore, a good property manager will not only help you with maintenance and other essential landlord roles. They will also assist you in screening better renters and keep your rent aligned with its market value.

As mentioned above, your property’s location plays an important role in evaluating it. Currently, some of the highly demanded areas in Egypt are:

These cities have high rent rates and the potential of a higher capital gain in case of selling as well, putting your mind at ease regarding capital growth vs. rental income indecision.

Final Thought

Whatever you decide regarding the capital growth vs. rental income dilemma, you would reap the benefits of your investment through choosing the right timing. Maybe even combining both strategies would guarantee you the highest ROI.

Nawy is your ultimate platform for buying and selling your property. If you are thinking of renting out your unit & don’t want the hassle of managing the property, check out Nawy Unlocked.

Don’t worry, Nawy can also help you sell your property with no hassle.

FAQs

What is rental yield?

Rental yield is the annual rental income of a property as a percentage of its market value or purchase price.

What is the difference between capital growth and income?

Capital growth is the gain of a property’s value over time, and it is an immediate capital gain when the unit is sold, while rental income is a passive, long-term, ongoing cash flow.

Do I pay tax on rental income?

According to the RTA, yes, you have to pay taxes, unless the annual rent is less than 24K EGP.